Circle IPO and the Casino Business

View Circle’s S-1 IPO Filing on the SEC Website

Circle and the Casino

How are we supposed to value Circle: as a bank or as a network? Their main product, USDC, the second-largest stablecoin in crypto after Tether, originated from the Centre Consortium, a 50/50 joint venture between Circle and Coinbase. The consortium was initially intended to support multiple stablecoin issuers over time. However, in August 2023, Circle bought out Coinbase’s stake in the consortium for $210 million in cash, along with 3.5% of Circle’s equity. Following this, Circle and Coinbase signed a new collaboration agreement that replaced the shared governance structure. The agreement formalized revenue sharing, designated Coinbase as a key business-to-business distribution partner, and granted it a worldwide, royalty-free license to use Circle’s branding and trademarks.

Since the split between Coinbase and Circle, Coinbase no longer holds any ownership in USDC but still receives a substantial annual payout from Circle, amounting to $908 million, or approximately 54% of Circle’s total revenue in 2024. While this might seem like an excessive amount to pay a single partner, it is important to keep in mind that Coinbase co-founded USDC, helped bootstrap its early network effects, and exchanged its prior governance stake for favorable economics. Meanwhile, Circle is pursuing new network effects, having paid Binance a one-time fee of $60 million, along with ongoing monthly incentives based on the amount of USDC held on Binance’s platform and in its treasury. Circle has also secured additional partnerships with Grab, Mercado Libre, and Nubank. Fintech companies often partner with big platforms or banks to scale quickly, but the platform capture more value than the fintech itself. The brand gets the trust, the user relationship, and a cut of the economics.

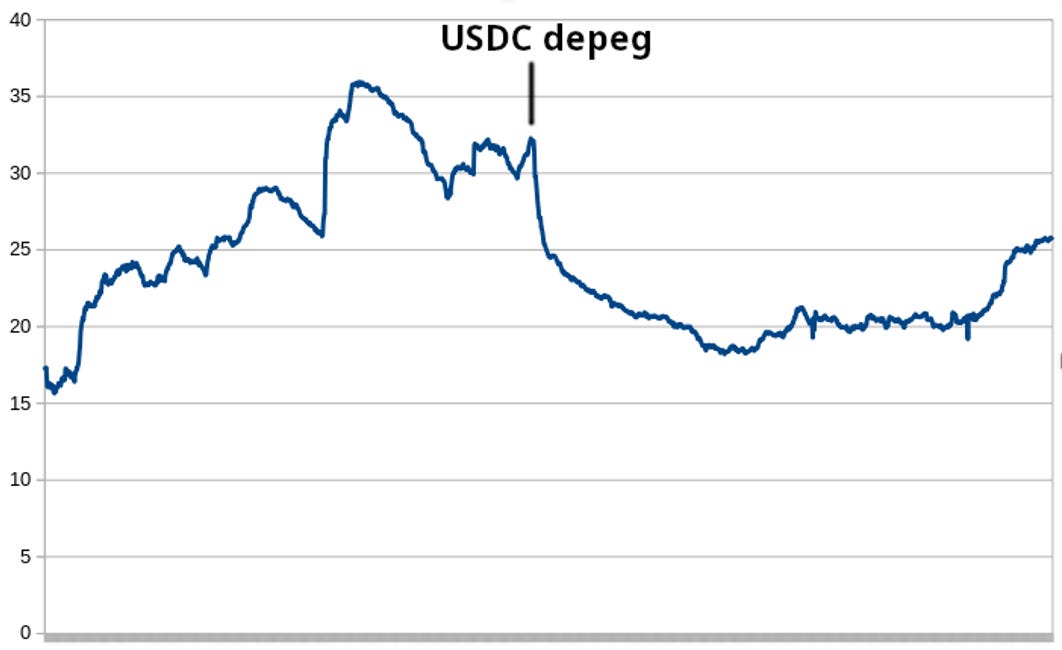

Circle has spent over half a billion dollars in operating expenses, not including marketing, technology, or product costs, yet its key metric, stalled between 2022 and 2024, with market share remaining flat at around 20 to 30 percent compared to its main competitor. In 2023, Circle lost over $600 million due to a 39% decline in USDC circulation following the collapse of Silicon Valley Bank and the resulting depegging event. The incident also reignited debate around the risks of limited banking access for crypto firms and the broader impact of U.S. regulatory uncertainty on the stability of the sector. As a counterbalance, Circle champions itself as a role model, having helped shape MiCAR in Europe and participated in the U.S. GENIUS and STABLE bills, while promoting USDC as a tool to preserve U.S. dollar dominance in the digital economy.

Circle’s IPO appears to be well-timed, but is it an exit strategy, or a serious push to further bootstrap network effects? Circle remains heavily reliant on net interest income, with projected revenue of $1.67 billion based on an average interest rate of 4.33%. A 100 basis point rate cut could reduce that figure by approximately $441 million. Meanwhile, upcoming stablecoin legislation signals a shift toward more serious business and could open the door for traditional banks (like Bank of America and Fidelity) to enter the stablecoin market. BlackRock, however, has already made its move, having secured contractual first-mover and early-warning rights on any material changes to Circle’s business. For now, the market may view Circle as the best pure play on the growing adoption of stablecoins. The passage of stablecoin bills could significantly increase the supply of USDC in circulation, and with it, Circle’s net interest income.

Coinbase monetizes USDC in an incredibly efficient way, as it is non-cyclical (unlike their trading business) and comes at little to no cost. The company is effectively using USDC yield as a customer acquisition tool: from its big fat paycheck of $908 million in earnings, it pays out approximately $224 million to users in interest. Coinbase has a strong incentive to grow USDC adoption, as its share of the revenue is lucrative, sticky, and increasingly becoming a core component of its growth strategy. This is why CEO of Coinbase Brian Armstrong is strongly advocating for allowing stablecoin issuers and platforms to pass interest directly to consumers for simply holding stablecoins. This stance is particularly interesting because Coinbase, which benefits financially from its arrangement with Circle, is attempting to influence regulation without directly bearing the regulatory burden itself. However, U.S. regulators appear to stay adamant with sticking to the same approach as their European counterparts under MiCaR, which prohibits yield-bearing stablecoins due to concerns that they could undermine monetary policy and financial stability.

Circle and the Coffeeshops

Coinbase and Circle know that the stablecoin itself isn’t the business, the network is. That is why Brian Armstrong is so eager to pass interest on to consumers to grow the network and why Circle is venturing off on their own to acquire distribution partners. Circle have been long known for wanting to entering the payments industry, but for stablecoins to reach their full potential a clearing system is required to solve the many-to-many problem between issuers and receivers of stablecoins. In today’s world, stablecoin recipients have to evaluate counterparty risk against the issuer (Circle) and the off-ramp (Coinbase) and contend with unfavorable accounting treatment. Currently corporations can not treat stablecoins as cash equivalents under current account standards (IAS7) but instead must handle them as financial instruments (IAS32) which creates a serious barrier to mainstream adoption.

Circle seeks to create competitive moats through bilateral acceptance agreements with for example Binance and Grab but in doing so, they are actually working against themselves and the overall health of the stablecoin ecosystem. Financial institutions, such as banks, require a mechanism to redeem fiat currency backing stablecoins from issuers with whom they do not and cannot have bilateral agreements with. Every payment network demands a clear and enforceable set of rules governing participant interactions. Such governance is typically established through a rulebook, similar to those used by SEPA or Visa, to which all participants agree to adhere at all times. This rulebook outlines participant eligibility, dispute resolution procedures, and compliance standards. This means all participants enter into legally binding agreements that incorporate the rulebook by reference. All participants must be properly identified, verified, and held accountable to contractual obligations, including liability for non-compliance. Only under these conditions can stablecoin payments truly become ubiquitous. However, developing this type of network is not in Circle’s core business.

So how should we value Circle: as a bank or as a network? Perhaps the real answer is somewhere in between. Circle's ambition to dominate stablecoin distribution is clear, but their reliance on expensive bilateral agreements and partnerships highlights the limits of their current approach. While Circle enjoys favorable economics in a high-rate environment, its heavy dependence on interest income and a few powerful platforms like Coinbase and Binance leaves it vulnerable. To truly unlock sustainable network effects, Circle might need to embrace building or contributing to an interoperable clearing infrastructure like a Visa or SEPA for stablecoins. However, developing such an ecosystem requires resources, patience, and incentives beyond Circle's current strategic direction. Ultimately, Circle’s future valuation hinges less on whether it behaves like a bank or a network today, and more on whether it can evolve into something greater: the critical infrastructure that connects the old financial system with the new digital economy.

Special thanks to the individuals listed below for their contributions to the discussion: @stablemaximus @matthew_sigel @Wyatt_Lonergan @shawnwlim @TheOneandOmsy @jamesjho_ @samkazemian @RyanWatkins_ @0xASK @riddle245 @inkymaze @kellyjgreer @sytaylor @SplitCapital @SGJohnsson @0xngmi @AlexH_Johnson @CampbellJAustin @nic__carter @robbiepetersen_ @LexSokolin @_TomHoward @bridge__harris @jerallaire @brian_armstrong